ACCA P2 Exam technique

摘要:【高顿ACCA小编】2015年 ACCA 考试即将开始,我们将第一时间公布考试相关内容,请各位考生密切关注高顿ACCA,预祝大...

【高顿ACCA小编】2015年ACCA考试即将开始,我们将第一时间公布考试相关内容,请各位考生密切关注高顿ACCA,预祝大家顺利通过ACCA考试。今天为大家带来的是 ACCA P2 Exam technique

( see also the section on general exam technique )

in the reading time read the requirements for all four questions – don‘t bother looking at the figures nor the notes relevant to the questions. Just read the requirements.

Q1 – what else is involved in the question as well as consolidations? What sort of consolidation is it – Statement of Financial Position, a Statement of Income with / without a Statement of Comprehensive Income, Statement of Changes in Equity, Statement of Cash Flows, a foreign consolidation?

the question often has five or six different parts to it – so what else is involved? Corporate governance? Environmental concerns? Ethics?

Q2 and Q3 – which Ass / IFRSs are being addressed in these two questions? Does either question ask for a report / memo? Correct style and persuasive content will be worth two to four marks

Q4 – what‘s current? Keep up to date with the examiner‘s articles – he writes quite frequently and very clearly. Personally I would in most cases try to avoid the 25 mark discussion question – it can be very difficult to accumulate sufficient points to earn even a bare pass mark of 13

where to start?

this is a matter of personal preference – having selected which question you are going to leave out, do you then start with a 25 marker, then question 1 and finish with the remaining 25 marker?

or do you head straight into question 1?

the only problem I can envisage with starting with question 1 is that it will be too easy to overrun your allocated time and thus steal time from the two 25 markers. Can you be strict with your self-discipline? If you are confident that you will not get pulled too deep into the figures in question 1, then go down that route

within question 1 itself, there will likely be four or five sub-questions. These mini-questions do not normally relate closely to the calculated solution which you are hoping to reach so….?

do these smaller part-questions BEFORE you get into the consolidation numbers – otherwise, you‘ll get swallowed up by the computations and never get to parts b, c, d and e! That‘s 15 marks gone!

should I write out a proforma first and then put in the easy figures?

there are NO marks for proformas! Statements of Financial Position, Income, Comprehensive Income, Changes in Equity, Cash Flows? NO MARKS FOR PROFORMAS!

sorry!

but calculate the goodwill correctly, or the Provision for Unrealised Profit ( PuP ), or interest paid for a cash flow – they will all score marks – even if you don‘t get round to putting them in a “final” Statement

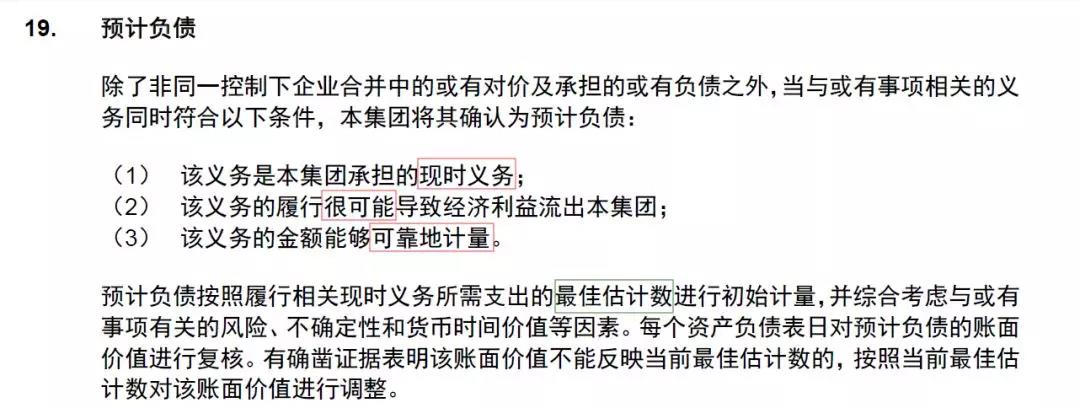

Q1

follow the OpenTuition lectures and set your workings out in consistently the same sequence – every time – you should find that that helps.

W1 – group structure

W2 – goodwill

then the PuP calcuation

W3a and W3b ( gain / loss on disposal / part disposal of subsidiary )

W3 – consolidated retained earnings

W4a – nci on the SoFP

W4b – nci on the SoI ( strictly, the SoCiEty )

W5a – investment in associate

W5b – our share of associate‘s this year‘s profits

reduce the problem to an automatic process and you should find it easier!

there are often 6, 7 or 8 paragraphs of notes at the end of the figures in Q1

start at the last one – say number 8

it often involves nothing at all – other than telling you the basis of the nci valuation at date of acquisition

then do number 7 – often some simple calculation like a dividend proposed but not yet accounted for

number 6 is often relatively straight forward as are also numbers 5, 4 and 3 – they will involve deciding whether a financial instrument should be valued at fair value, whether a potential liability should be accrued, whether an asset needs to be impaired, whether inventory value needs adjusting or whether revenue should be recognised on a basis different to the existing basis.

these are not intended to be a comprehensive list of possible adjustments – merely illustrative of the sort of matter you could expect to find

each of these notes requires a clear working to explain / calculate the amount and effect of the adjustment necessary

this should now leave you with just numbers 1 and 2 which typically will give you the information about the acquisition / disposal of the subsidiary and the associate

DO NOT get stopped by any single note – if you can‘t do it – LEAVE IT and come back later when you have picked up the marks you can collect

when you do come back to it, if you still cannot manage to find a solution, then GUESS – but do not be tempted to start verbal explanations to the marker about what / why / how you have arrived at the guessed figure – simply put “say $50,000”

Q2 and Q3

establish the style which has been required – report / memo or letter or simply a comment on the directors‘ choice of accounting treatment – more often than not, they are incorrect, but not always!

typically the questions will be sub-divided into four or five parts

make sure that you correctly allocate your time to allow a reasonable effort at ALL parts of the question

Q4

current affairs

the examiner has said that he will examine each new IFRS at the earliest opportunity

so keep your eye on the accountancy press and Student Accountant

occasionally, question 4 has a computational element but, more often than not, it‘s pure discussion

personally, nine times out of ten, I would avoid it

it is excessively difficult to produce 25 markable points in a discussion within 45 minutes

it‘s difficult to produce half that number, yet that is what you need to get a passing grade on this question

if you really do have to attempt question 4, follow the usual rules about planning what you are going to write. This becomes particularly relevant when you are tackling a question about which you could very well know not much at all

remember, each valid point should be earning a mark for you

your target is therefore to think, plan and write 25 markable points

ok, you won‘t achieve that, but at least let that be your target

the examiners like the answers to be subdivided into sections with appropriate headings

本文由高顿ACCA编辑整理,转载请注明出处